Why the Trump Pandemic and Market Crash Mean Everyone Should Think Like a Central Banker

Bailing banks out? Again? Really?

Trillions of dollars provided by the Federal Reserve to keep banks out of trouble should sound familiar and it’s an anger trigger for many.

During the Great Recession, the mighty Fed reached out with greenback-stuffed lifesavers for the giant financial institutions whose misfeasance, malfeasance and nonfeasance brought on the calamity. While Too-Big-to-Fail bank executives pocketed multi-million-dollar bonuses in 2008 as Mother Jones, CBS News and others documented, millions of regular folks lost their homes despite promises of help that turned out mostly to be hollow.

This year, the Federal Reserve put in trillions of dollars in the hands of bankers, extending credit and adding liquidity to markets at least 20 times in March, according to the Fed’s own announcements.

A combination of cheap credit, regulatory relaxation

and increased purchases of bonds (which put cash into the market) is bound to seem like another giveaway.

But this is 2020, not 2008, and no matter how mad the Fed’s actions make you feel, you’d better hope it works. To understand why, you’ve got to think like a banker.

Keep in mind that the Fed’s actions are not the same as those of Congress and Donald Trump in giving bailouts to airlines and other industries using money borrowed against your future tax dollars. The Fed isn’t part of the federal spending that Congress approves.

Liquidity Is Vital

Liquidity is like a body’s circulatory system, only for financial systems. Adam Smith taught us that more than 200 years ago in the first book to explain market economies, The Wealth of Nations. When your blood flow stops. you die; when cash flow shrivels, economies collapse.

When liquidity disappears, everything financial freezes. You get 2008 again. If nothing is done quickly to restore cash flow, you get the Great Depression 2.0.

Think of families constantly bringing money in, putting it away, then sending it out again. Banks, hedge funds, pension funds, insurance companies, mutual and money market funds and other financial institutions constantly move money. That’s how business and life work. Institutions invest in one place, close out positions in another, pay bills, distribute pension checks, put some in savings.

Some days these big institutions have more cash than they need. When that happens, they typically park the extra cash in U.S Treasury bonds and notes, which are considered the safest investment vehicles in the world. Backed by the full faith and credit of the U.S. government, whose dollar is the world’s reserve currency, Treasurys are central to the smooth and dependable flow of cash. That flow is known as liquidity.

Constant Churn of Cash

On other days, of course, banks and other financial concerns need to meet payroll, pay taxes and make other expenditures, even when they don’t have enough cash on hand. Fortunately, there is the secondary market to convert Treasurys to cash and a repo market, standing for repurchase agreement, both of which help keep money flowing.

The repo market is like borrowing $10 from Felix at work to pay for lunch with the promise that you’ll return it the next day when your paycheck is issued. Now just add lots of zeros to the size of that short-term loan.

Banks are supposed to lend to one another this way. The Fed’s target funds interest rate range, in theory, governs this borrowing between banks. Right now that range is from zero to a quarter of one percent—in essence, between interest-free and almost interest-free money.

Corporations, Too

There is also secured repo market. It involves many more types of institutions than banks.

Corporations that need cash, for example, often will offer Treasurys as collateral for a short-term loan. The interest rates on these loans can vary more but typically fall in and around the Fed’s target range.

The important thing is that everything is fine so long as the money keeps moving. But when it stops, like during the height of the 2008 financial collapse, disaster happens. Companies suddenly can’t meet payroll or pay their taxes. Similarly, pension funds can’t make payments to retirees unless they can convert the stocks and bonds they own into cash.

Pre-Pandemic Rumblings

Warning signs that liquidity was icing up began flashing last year, before even the medical experts were aware of this novel virus that has us sheltering in our homes hoping the tiny bug passes us by.

Starting in 2019 and extending into 2020, strange and bad things began to happen when it comes to the flow of cash.

While some repo agreements were at or near the interest rates set by the Fed, some loans spiked at interest rates more than four times as high. That’s about as rare as snow in New Orleans.

Such interest rate spikes in commercial lending send a warning signal to banks that normally would have little concern extending short-term loans to other banks and corporations to keep the cash flowing. Those flashing red lights suggest to the banks that some loans might not be paid back in full or, even worse, at all.

Fear of Loan Defaults

The signals this year show how concerned bankers are viewing the economic damage from the coronavirus and the greater risk that borrowed money may not be paid back in full, on time and with interest.

When the top interest rates for repo agreements secured by Treasurys and other sound assets soar far above the Fed’s interest rate range, two problems can occur.

One is that banks with extra money to lend may get worried and move away from repo agreements, reducing the options for companies and other institutions to get cash as needed. That pulls out a prop supporting the entire banking system.

Banks have the option of borrowing overnight from the Fed at higher rates than the target rates, but the Fed looks to be the lender only of last resort. Going too often to the Fed window, as it’s known, reasonably raises suspicions about how sound a bank is, inviting audits and other regulatory scrutiny. Or at least it should.

When Banks Need Cash

Another problem is that the situation could mean some of the biggest banks don’t have enough liquidity—free money, again—to lend. Less cash to lend across all the banks means there isn’t enough cash supply. Classic economics says more demand than supply means higher prices and, in this case, higher interest rates for institutions borrowing from banks.

There was another major telltale sign that really picked up this year. Liquidity in the secondary Treasurys markets began freezing up, locking everyone in place like a boat in a frozen lake.

First, stock prices started plummeting. All sorts of investors, particularly big ones, decided to look for safety by selling risky stocks and buying presumably safe Treasurys.

The surge of cash out of stocks pushed up the prices of Treasurys. When you pay more for a Treasury you get a lower interest rate than the interest rate promised to the initial buyers. Think of a $1,000 bond whose price rises to $1,100. If you were supposed to get 2% interest now you will get only 1.8% because the Treasury still pays only what it originally said it would.

Next, the spread between how much buyers were willing to pay (the “bid”) and the amount sellers were willing to take (the “ask”) got wider. Suddenly, holders of Treasurys couldn’t get close enough to what they wanted for those securities, so they held onto them. That meant banks and companies needing to make payroll and other expenses didn’t have enough cash.

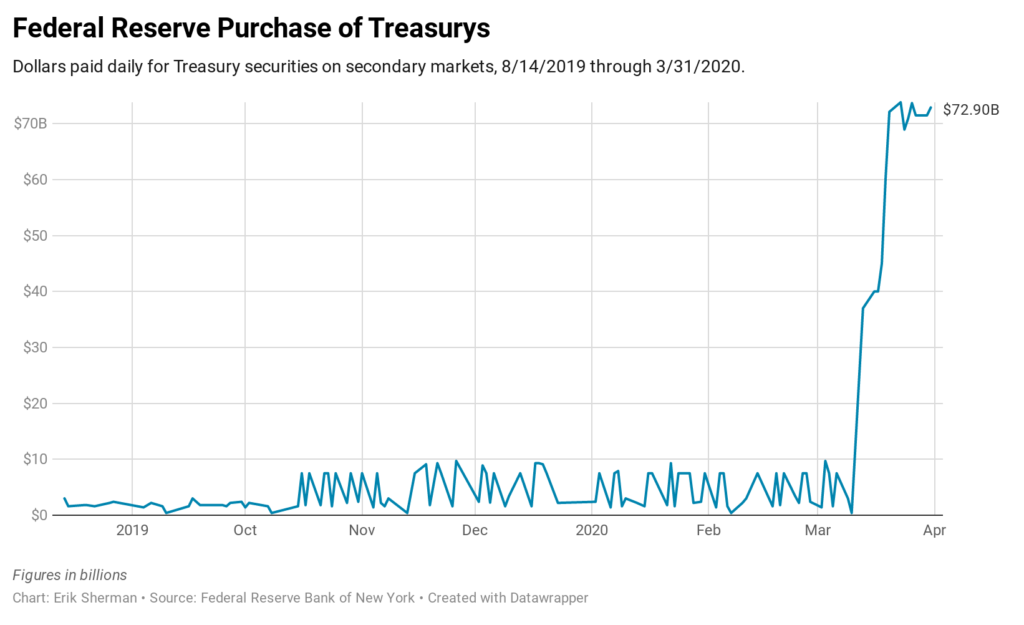

This threatened to freeze the Treasurys markets, which in turn would help bring commerce across the globe to a halt. So, the Fed started buying Treasurys—a massive amount of them, as the earlier graph shows. Between August 14, 2019, and March 31, 2020, the Fed bought $1.24 trillion—with a “t”—in Treasurys, injecting massive amounts of additional liquidity.

The Fed’s Money Doesn’t Come from Taxpayers

You probably didn’t want to see bailouts coming. Nobody did, easy as it is to get angry over any financial help going to Wall Street. Even big investors and bankers are much happier when systems work as expected.

But to look back at the financial collapse and decide to stick it to the banks is about as classic an example of the old saying “cutting off your nose to spite your face” as you could find. Let things freeze up and the result would likely be a swift, deep and long economic collapse that no one has seen since the Great Depression. It could even be worse.

Yes, really that bad.

If there’s any silver lining, it’s in addressing the anger many have expressed online that these titanic amounts of money will come out of taxpayers’ pockets and force many useful parts of the federal budget to be struck.

The worry is misplaced.

The Fed doesn’t work from tax revenues. It’s not part of the federal budget. It is, however, one of the major monetary referees in the world. When it buys securities or lends money to banks or other groups, it creates money by adjusting figures in electronic ledgers. Eventually, this newly created money comes back in, with interest, and the Fed readjusts its ledgers again.

Nothing is being taken from the budget because it’s all a matter of trust.

And let’s hope the trust continues or else we all have a bigger problem than loans at zero interest which keep cash flowing throughout the economy.